The GLP-1 Gold Rush: The $178 Billion Transformation of Obesity and Metabolic Healthcare

GLP-1 receptor agonists have moved from diabetes treatment discussions into the center of healthcare innovation, pharmaceutical investment, and preventive metabolic care.

Trend Analysis

A decade ago, GLP-1 receptor agonists were largely confined to diabetes treatment discussions. Today, they sit at the intersection of healthcare innovation, pharmaceutical investment, and preventive medicine.

The global GLP-1 receptor agonists market is projected to reach $178.4 billion by 2030, expanding at a CAGR of 18.4%. As obesity rates continue to rise globally and healthcare systems increasingly prioritize preventive and metabolic care, GLP-1 therapies are becoming strategic assets for pharmaceutical companies, healthcare providers, payers, and investors.

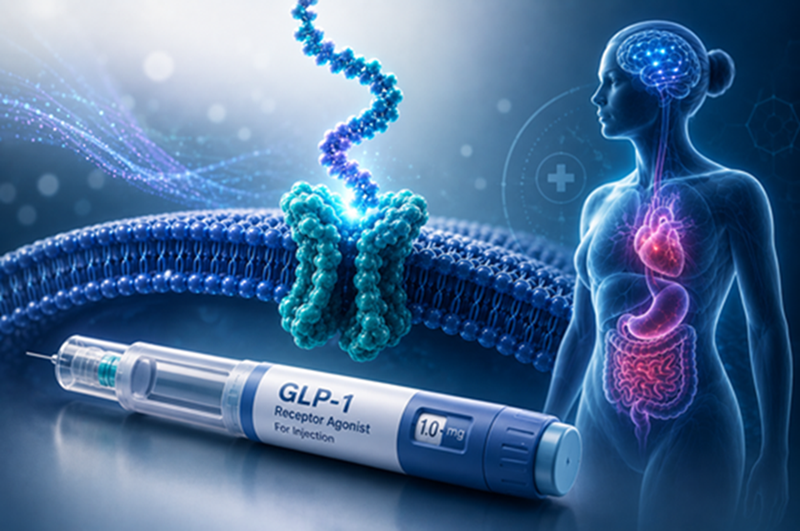

What are GLP-1 receptor agonists?

GLP-1 receptor agonists are medications designed to mimic the action of glucagon-like peptide-1, a naturally occurring hormone that regulates blood sugar, appetite, insulin secretion, and gastric emptying.

These therapies help patients manage Type 2 diabetes while also promoting significant weight loss and metabolic improvements. Common GLP-1 receptor agonists include semaglutide, liraglutide, dulaglutide, and exenatide.

Why the market is scaling so quickly

- Global obesity crisis: Rising obesity prevalence is creating a substantial addressable patient population, while GLP-1 therapies have demonstrated clinically meaningful and sustained weight reduction.

- Expanding clinical applications: Beyond diabetes and obesity, GLP-1 therapies are being evaluated for cardiovascular risk reduction, metabolic syndrome, chronic kidney disease, and potential neurological applications.

- Shift toward preventive healthcare: Health systems are moving from treatment-based models toward prevention-oriented strategies that address metabolic dysfunction earlier.

- Pharmaceutical innovation and investment: Major pharmaceutical companies are investing in next-generation obesity and metabolic therapies, including oral delivery systems and combination treatments.

Regional market dynamics

North America remains the largest market, projected to grow to $82.43 billion by 2030. Strong healthcare spending, favorable reimbursement structures, and early adoption of obesity therapeutics continue to support regional growth.

Asia Pacific is expected to record the highest CAGR of 23.6% from 2025 to 2030. Rising obesity prevalence, increasing healthcare investments, and improving access to advanced therapeutics are driving regional expansion.

Industry trends shaping the next phase

The next phase of growth will likely come from expanded indications beyond diabetes and obesity. Researchers are evaluating GLP-1 therapies for cardiovascular protection, kidney disease management, and neurological disorders.

Oral formulations are expected to improve patient adherence and broaden market accessibility, while dual and triple receptor-targeting therapies may provide superior metabolic outcomes compared with traditional GLP-1 treatments alone.

Digital health platforms and AI-powered monitoring solutions are also being integrated with obesity and diabetes treatment pathways, improving patient engagement and treatment outcomes.

Regulatory landscape and emerging risks

The rapid rise in demand has created new regulatory challenges. The U.S. Food and Drug Administration has repeatedly expressed concerns regarding unapproved and compounded GLP-1 products marketed for weight loss.

For pharmaceutical manufacturers and healthcare providers, compliance, product quality, and patient safety will remain critical success factors as regulatory scrutiny intensifies.

Competitive outlook

The GLP-1 market currently exhibits relatively limited rivalry compared with many mature pharmaceutical categories. However, this dynamic is expected to change as new entrants, biosimilars, and next-generation metabolic therapies enter the market.

Competitive advantage will increasingly depend on clinical efficacy, manufacturing scale, regulatory approvals, supply chain resilience, market access, reimbursement strategies, and physician and patient engagement.

Strategic outlook for stakeholders

What began as a breakthrough in diabetes management has evolved into one of the most consequential healthcare opportunities of the decade. Metabolic health is becoming a strategic priority for providers, pharmaceutical companies, investors, and governments.

As the market advances toward $178 billion by 2030, GLP-1 therapies are set to redefine healthcare economics, influence treatment standards across multiple disease areas, and establish themselves as one of the most transformative therapeutic categories of the modern era.

Frequently asked questions

- What are GLP-1 receptor agonists used for? They are primarily used for Type 2 diabetes management and obesity treatment, helping regulate blood sugar, reduce appetite, and support weight loss.

- Why is the GLP-1 market growing? Growth is driven by rising obesity prevalence, expanding clinical applications, increasing healthcare investments, and strong pharmaceutical innovation.

- Which region is growing fastest? Asia Pacific is projected to be the fastest-growing regional market, with a CAGR of 23.6% between 2025 and 2030.

- What is the future size of the GLP-1 receptor agonists market? The market is expected to grow from $76.7 billion in 2025 to approximately $178.4 billion by 2030.

Operationalize This Insight

Looking to evaluate GLP-1 and metabolic healthcare opportunities? Preonz structures market size, regional demand, regulatory pressure, and competitive positioning into decision-ready intelligence.